NOT FOR RELEASE, PUBLICATION OR DISTRIBUTION IN WHOLE OR IN PART IN OR INTO THE UNITED STATES

Sequoia Economic Infrastructure Income Fund Limited ("SEQI" or the "Company")

Monthly NAV and portfolio update - June 2025

The NAV per share for SEQI, the largest LSE listed infrastructure debt fund, increased to 92.56 pence per share from the prior month's NAV per share of 91.79 pence, representing an increase of 0.77 pence per share.

|

|

pence per share |

|

31 May NAV |

91.79 |

|

Interest income, net of expenses* |

0.52 |

|

Asset valuations, net of FX movements |

0.23 |

|

Subscriptions / share buybacks |

0.02 |

|

30 June NAV |

92.56 |

No expected material FX gains or losses as the portfolio is approximately 100.1% currency-hedged. However, the Company's NAV may include unrealised short-term FX gains or losses, driven by differences in the valuation methodologies of its FX hedges and the underlying investments - such movements will typically reverse over time.

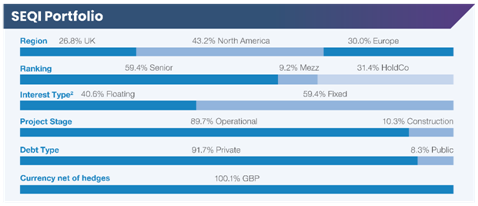

Well positioned to benefit from high interest rates; 59.4% of portfolio is in fixed rate investments as of June 2025.

Investor updates - Annual Report FY25

The Investment Adviser is pleased to announce that its Annual Report and Sustainability Report for the year ended 31 March 2025 were both released on 25 June 2025.

Annual Report: Results Centre - Sequoia Economic Infrastructure Income Fund Limited

Sustainability Report: Publications - Sequoia Economic Infrastructure Income Fund Limited

Market Summary

Tariff Impact & Geopolitical Analysis

|

· |

On 7 July (after month-end), President Trump dispatched letters to key trading partners, including Japan and South Korea, announcing tariffs ranging from 25% to 40% effective 1 August. This move effectively extends the negotiation deadline from 9 July to 1 August.

|

|

· |

The U.S. has also signalled a willingness to negotiate exemptions on a country-by-country basis. This emphasis on deal-making over blanket implementation has provided a degree of reassurance to markets, with cautious optimism for a more measured and negotiated trade environment.

|

|

· |

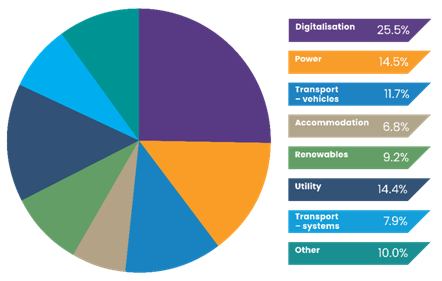

Infrastructure is broadly recognised as a defensive asset class, typically exhibiting resilience during periods of market volatility. SEQI's portfolio is deliberately constructed to reflect this, with minimal exposure to more cyclical subsectors such as oil refining, aviation, and container ports. As of June 2025, 55.9% of the Company's investments are concentrated in traditionally defensive assets, including renewables, digital infrastructure, utilities, and accommodation.

|

*Capital movements includes an element of capitalised interest.

Interest Rate Announcements and Inflation Data

|

· |

During June, The Federal Reserve held rates steady at 4.50% and is expected to begin easing policy rates later in Q3. The Bank of England maintained its policy rate at 4.25%, though markets increasingly anticipate a 0.25% rate cut in September. The European Central Bank reduced its policy rate from 2.25% to 2.0%, as inflation in the Eurozone eased to 1.9%, below the ECB's 2% target.

|

|

· |

The yield on the 10-year U.S. Treasury ranged between 4.2% and 4.5% during June. This volatility stemmed from persistent trade concerns, fiscal policy uncertainty, and the market's reassessment of future U.S. inflation. By June month-end, the yield settled at 4.25%, approximately 0.15% - 0.20% below May levels, indicating a softening of rates at the short end of the curve.

|

|

· |

U.K. sovereign yields followed a similar path. The 10-year U.K Gilt yield declined by approximately 0.15% to 4.5% by the end of the month, but spiked to 4.6% after June month-end, in the aftermath of the welfare reform vote. The 10-year German Bund yield fluctuated between 2.5% and 2.6% during June.

|

|

· |

In the near term, de-escalation of trade tension is expected to help ease inflationary pressures. While the more recent tariffs are aggressive in scope, the U.S. has left room for diplomacy, signalling that countries entering trade talks before the 1 August deadline could secure allowances or avoid the new measures altogether, which should further reduce inflationary pressures.

|

|

· |

As inflation gradually abates over time, the likelihood of future interest rate cuts increases, making alternative investments such as infrastructure more attractive when compared to liquid debt. While the pace and size of interest rate cuts will vary across the Company's different investment jurisdictions, the general consensus remains one of declining interest rates throughout the year.

|

Portfolio Update - June 2025

Revolving Credit Facility and Cash Holdings

|

· |

As of June 2025 month-end, the Company had drawn £94.7 million on its revolving credit facility of £300.0 million and had cash of £38.7 million (inclusive of interest income), and net undrawn investment commitments of £73.6 million.

|

Portfolio Composition

|

· |

The Company's invested portfolio consisted of 55 private debt investments and 5 infrastructure bonds, diversified across 8 sectors and 29 sub-sectors.

|

|

· |

59.4% of the portfolio is comprised of senior secured loans reflecting the Company's defensive positioning.

|

|

· |

It had an annualised yield-to-maturity (or yield-to-worst in the case of callable bonds) of 9.86% and a cash yield of 7.34% (excluding deposit accounts).

|

|

· |

The portfolio pull-to-par, which is incremental to NAV as loans mature, is 4.3 pence per share as of June 2025.

|

|

· |

The weighted average loan life is 3.3 years as of June. This short maturity profile means that as loans mature, the Company can take advantage of new lending opportunities.

|

|

· |

Private debt investments represented 91.7% of the total portfolio, allowing the Company to capture illiquidity yield premiums.

|

|

· |

The Company's invested portfolio currently consists of 40.6% floating rate investments and remains geographically diversified with 43.2% located across the U.S., 26.8% in the U.K. and 30.0% in Europe.

|

Portfolio Highly Diversified by Sector and Size

Share Buybacks

|

· |

The Company bought back 2,063,828 of its ordinary shares at an average purchase price of 80.75 pence per share in June 2025.

|

|

· |

The Company first started buying back shares in July 2022 and has bought back 224,629,202 ordinary shares as of 30 June 2025, with the buyback continuing into July 2025. This share repurchase activity by the Company continues to contribute positively to NAV accretion.

|

New Investment Activity During June 2025

|

· |

A senior loan for £18.7 million to Community Fibre Limited. SEQI has committed £45 million of a £125 million financing facility to support the borrower's continued expansion across London.

|

|

· |

An additional senior loan to GenOn Bowline Power LLC for $1.8 million. The borrower is an electricity generator based in New York, USA. The total position size on this loan was $28.4 million as of June 2025. |

|

|

|

No investments repaid during June 2025.

Non-performing Loans

The Company continues to work towards maximising recovery from the non-performing loans in the portfolio (equal to 0.9% of NAV): There are no new announcements this month.

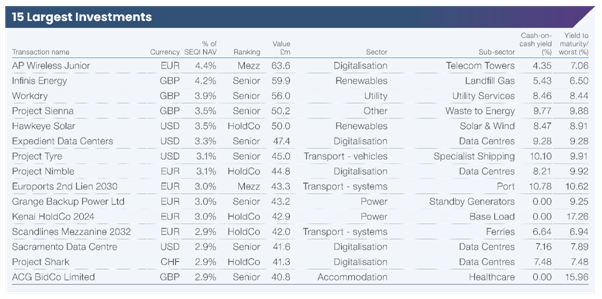

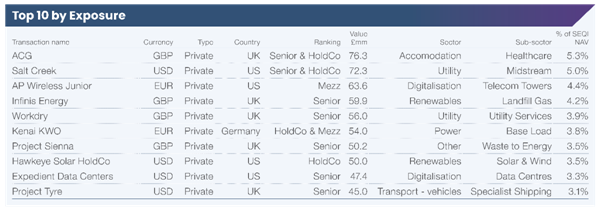

Top Holdings

Valuations are independently reviewed each month by PWC.

Full list of SEQI's Portfolio Holdings and SEQI Monthly Factsheet:

http://www.rns-pdf.londonstockexchange.com/rns/0165R_1-2025-7-14.pdf

http://www.rns-pdf.londonstockexchange.com/rns/0165R_2-2025-7-14.pdf

About Sequoia Economic Infrastructure Income Fund Limited

|

· |

SEQI is the U.K.'s largest listed debt investor, investing in economic infrastructure private loans and bonds across a range of industries in stable, low-risk jurisdictions, creating equity-like returns with the protections of debt. |

|

· |

It seeks to provide investors with regular, sustained, long-term income with opportunity for NAV upside from its well diversified portfolio. Investments are typically non-cyclical, in industries that provide essential public services or in evolving sectors such as energy transition, digitalisation or healthcare. |

|

· |

Since its launch in 2015, SEQI has provided investors with ten years of quarterly income, consistently meeting its annual dividend per share target, which has grown from 5p in 2015 to 6.875p per share in 2023. |

|

· |

The fund has a comprehensive ESG framework combining sustainability goals, a proprietary ESG scoring methodology, alongside processes and metrics with alignment to key global initiatives. |

|

· |

SEQI is advised by Sequoia Investment Management Company Limited (SIMCo), a long-standing investment advisory team with extensive infrastructure debt origination, analysis, structuring and execution experience. |

|

· |

SEQI's monthly updates are available here: Monthly Updates - seqi.fund/investors/monthly-updates |

|

|

|

For further information please contact:

|

Investment Adviser Sequoia Investment Management Company Limited Steve Cook Dolf Kohnhorst Randall Sandstrom Anurag Gupta Matt Dimond |

+44 (0)20 7079 0480 |

|

|

|

|

|

|

|

|

Joint Corporate Brokers and Financial Advisers Jefferies International Limited Gaudi Le Roux Harry Randall |

+44 (0)20 7029 8000 |

|

|

|

|

|

||

|

J.P. Morgan Cazenove William Simmonds Jérémie Birnbaum

|

+44 (0)20 7742 4000 |

|

|

|

Public Relations Teneo (Financial PR) Elizabeth Snow Colette Cahill

|

+44 (0)20 7260 2700 |

|

|

|

Alternative Investment Fund Manager (AIFM) FundRock Management Company (Guernsey) Limited Dave Taylor Chris Hickling

|

+44 (0)20 3503 600 |

|

|

|

Administrator / Company Secretary Apex Fund and Corporate Services (Guernsey) Limited

|

+44 (0)20 3503 600

|

|

|

|

|

|

|

This announcement is not for publication or distribution, directly or indirectly, in or into the United States of America. This announcement is not an offer of securities for sale into the United States. The securities referred to herein have not been and will not be registered under the U.S. Securities Act of 1933, as amended, and may not be offered or sold in the United States, except pursuant to an applicable exemption from registration. No public offering of securities is being made in the United States.

RNS may use your IP address to confirm compliance with the terms and conditions, to analyse how you engage with the information contained in this communication, and to share such analysis on an anonymised basis with others as part of our commercial services. For further information about how RNS and the London Stock Exchange use the personal data you provide us, please see our Privacy Policy.